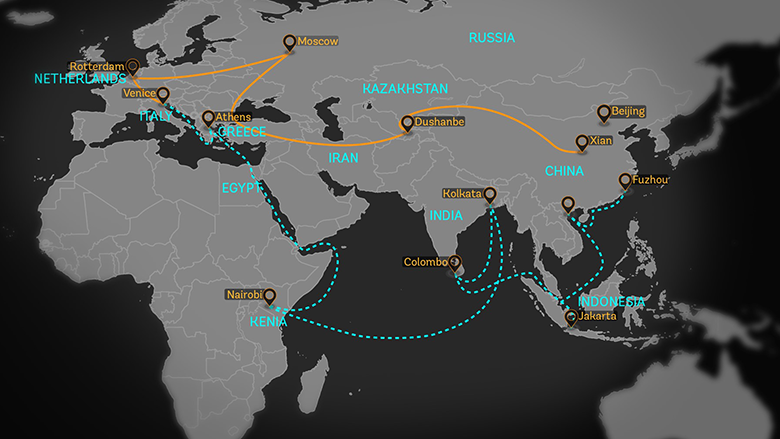

Much has already been written on the objectives of the Belt Road Initiative (BRI) from the Chinese viewpoint. They range from providing game-changing geostrategic leverage and even military access in many countries in China’s neighbourhood to a more narrow purpose of selling Chinese surplus steel, cement and construction capacity on credit to countries that are resource-strapped for developing their infrastructure. Opinions from the perspective of the recipient country are also equally divergent: from a ticking time-bomb of burgeoning external debt to a much-needed external funding source which will supplement the role of the multilateral and regional lenders in promoting investment and trade.

Post Covid, this strategic economic initiative is in trouble for a number of reasons, such as the finances of partner countries

One has also come across elegant research studies on the benefits of BRI, including the articulation and estimation of its positive externality for the recipient countries. A good number of those researches have been sponsored and funded by the Confucian Institute, which also endeavours to expand the envelope of BRI’s impact to include more lofty things such as inclusive globalisation, culture, innovation, talent development etc. But progress is uncertain at best and faces new challenges given the changes in the economic scenario caused by the impact of COVID-19, the slowdown that began even before that and the changed global perception of China.

A meaningful mid-term performance review of BRI covering its financial aspects and its impact on the global institutional arrangements for project funding is not easy, for two reasons: One, the Chinese side never provide comprehensive information on, even on an aggregate basis, the quantum of loans approved by the its lenders, progress of loan recovery and realised return on investments. Two, the loan recipients reveal even less. One still remembers the deadlock in the emergency loan negotiations between Pakistan and IMF in 2018-19 over the issue of disclosing the amortisation schedule of the former’s China Pakistan Economic Corridor, or CPEC-related debt to China.

Top-down policy

The stated intentions of BRI to reach US$4 trillion in financed projects are far higher than the projects currently under development, worth about US$ 230 billion. China expects that its own companies will plan, construct and supply the projects it funds. However, because of its wide scope, gigantic scale and very ambitious timelines, the Chinese authorities have been facing a challenge to ensure that the selection of countries and the projects satisfies the strategic policy goals decided at the top by the Communist Party of China (CPC).

The stated intentions of BRI to reach US$4 trillion in financed projects are far higher than the projects currently under development, worth about US$ 230 billion.

While it is clear that identification of big-ticket projects in countries of significant strategic importance to China requires prior CPC clearance, for others it’s a bit chaotic and messy. Almost all the documents released by state-owned financial institutions that have been pressed into service for BRI never fail to mention that their choice of projects must take into account “Chinese perspective and national interest” and follow “China-specific governance mode”. The ambiguity of these words for analysts and others in these institutions who support decision-making at higher levels has been sought to be addressed in a manner typical of China: by way of indoctrination. In China Investment Corporation (CIC), the largest Sovereign Wealth Fund (SWF) of China with assets over US$ 1 trillion, for example, 906 of its staff attended training programmes in 2018 on ‘Ideals and Beliefs’, vis-à-vis 1,150 who were trained ‘investment capabilities’, according to the CIC. The Silk Road Fund, the other SWF, created in 2014 with a corpus of US$ 40 billion for BRI funding, does not publish any financial statement. CIC doesn’t disclose its total loans, there are no details provided on any of its asset/liability and income/expenditure items, and so on.

Multilateral Development Banks (MDB) and BRI

China has been critical of the poor performance of Multilateral Development Banks (MDBs) in financing infrastructure projects in developing countries. It has thus echoed the concerns of infrastructure-deficit countries in this regard. However, China’s viewpoints on this issue have also been shaped by two other factors: One, China feels frustrated that its weight in World Bank and Asian Development Bank are not commensurate to its economic and financial heft. Two, China feels that international financial institutions, in general, are evolving slowly and that it would like their pivot to shift from the west towards itself. China’s latest 5-year Plan lists its ambition “for the creation of a financial cooperation platform that is open, pluralistic, and mutually beneficial”.

China has been critical of the poor performance of Multilateral Development Banks (MDBs). While the high cost structure of MDBs and the tardy pace at which project appraisals happen there are indefensible, credit must be given for their sustained emphasis on governance, environmental and gender equality issues.

While the high cost structure of MDBs and the tardy pace at which project appraisals happen there are indefensible, but credit must be given for their sustained emphasis on governance, environmental and gender equality issues. For all we know, China’s support for even its own variety of corporate governance is tactical, at best, especially in BRI projects. A case in point is the on-going multipurpose road-rail bridge on the Padma in Bangladesh, which is a US$ 3.6 billion BRI project. Originally, the project was to be financed by World Bank, which subsequently refused to sanction the loan alleging “high-level corruption conspiracy” in the selection of the vendor for project preparation. Now, China Major Bridge Engineering Company is the main contractor. Interestingly, although two non-Chinese construction companies had also purchased papers when the tender for the project was floated in early 2014, only the Chinese company submitted both technical and financial bids.

Still another is the recent revelations made by the anti-corruption agency of Pakistan about payments in the range of US$300-400 million made to two flagship BRI thermal power companies there based on fraudulent interest cost claims. Needless to say, there was systematic collusion among all concerned in giving such profitable deals to the Chinese sponsor entities. It is a common knowledge in Pakistan that cost of BRI thermal power projects in that country are inflated by 30-40%.

Covid-19 pandemic and BRI

Like all infrastructure projects elsewhere, progress of those under BRI has considerably slowed due to the pandemic. And the recipient countries, for many of whom the priorities now stand shifted to health services and health infrastructure, have already begun a clamour for relaxation of debt repayment terms. While CPC is likely to accommodate this to some extent and also offer projects under the latest avatar of BRI – Health Silk Road and Digital Silk Road – the impact of all this is likely to be a huge negative for the state-owned financial institutions. China would do well to remember a simple truism of banking: if state-owned banks/shadow-banks are pushed by the state to take larger and larger risks, one day they will prove to be an Achilles heel for the state itself. Viewed from this angle, CPC has reasons to feel concerned now at the uncertain future progress of its most ambitious foreign and economic policy initiative.

(Himadri Bhattacharya is a former central banker and a consultant to the IMF)